Peter Thiel Isn’t the First Person to Invest in a Lawsuit

Peter Thiel Isn’t the First Person to Invest in a Lawsuit

Tuesday night, a bizarre twist emerged in the already-weird story of ex-professional wrestler Hulk Hogan’s lawsuit against the provocateurs of Gawker, who published an excerpt of his leaked sex tape: Forbes revealed that Hogan’s legal fees had been paid by billionaire PayPal founder and libertarian Peter Thiel. Yesterday, Thiel confirmed that he’s been waging a campaign on behalf of the many “victims” of Gawker Media, a company that publicized the open secret that he was gay in 2007. This is “one of my greater philanthropic things that I’ve done,” he told the New York Times. “It’s safe to say this is not the only” case in the works.

While Thiel is unusual in subsidizing lawsuits for the purpose of revenge (or, as he considers it, philanthropy), litigation financing is a thriving sector where investors front the costs of expensive lawsuits in exchange for a piece of a lucrative settlement. The practice has been around since almost as long as there’ve been courts. It’s been controversial for just as long.

In antiquity, Greeks and Romans frowned on the practice and tried to restrict it. In medieval times, as the English nobility slowly moved from slaughtering to suing each other, barons began subsidizing their vassals’ legal cases in order to swamp their opponents with litigation. The practice was duly banned in the 13th century, but in modern times attitudes began to shift. The UK lifted the ban in the 1960s; in 1997, the Massachusetts Supreme Judicial Court made a ruling that paved the way for today’s litigation financing, citing a “fundamental change in society’s view of litigation — from a social ill, which, like other disputes and quarrels, should be minimized, to a socially useful way to resolve disputes.” Other states soon followed, and in the ensuing decades there’s been a boom in litigation funding, particularly for commercial law and personal injury cases, with their high payouts, legal costs in the millions and multi-year timelines.

Historically, plaintiffs who didn’t qualify for legal aid or pro bono representation would seek out investors, who would evaluate the risk of the investment on a case-by-case basis. Today, investors aren’t necessarily waiting for clients to come to them. According to Virginia personal injury lawyer Matthew Kreitzer, some hedge funds are essentially asking law firms, “‘Look, we want to invest in personal injury cases. Can we give you money to go out and get some?’”

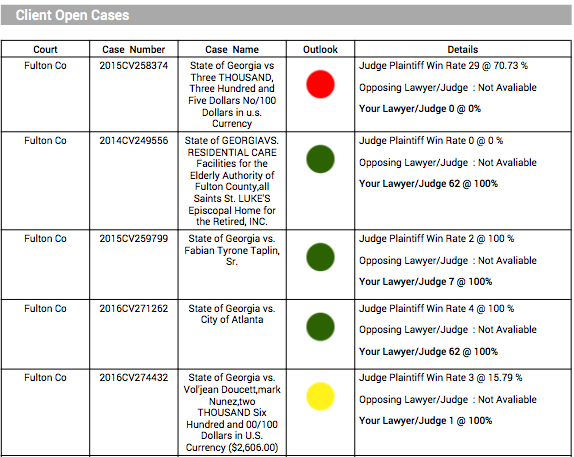

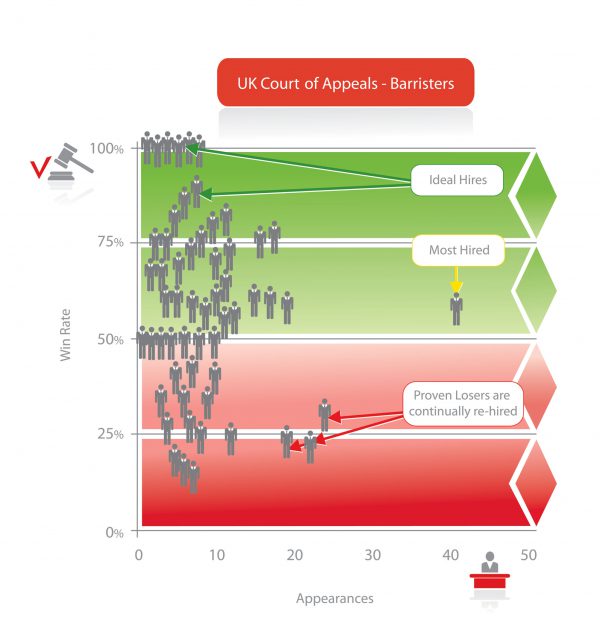

As hedge funds put more resources into litigation financing, they’re commodifying the practice as an investment vehicle and minimizing risk by relying less on legal instincts about a specific case and more on data. “At the intersection of litigation and finance, you get people from both litigation and finance involved, neither understanding the other side,” says Toby Unwin, chief innovation officer at the big data firm Premonition. He’s trying to bridge that gap, helping lead his company’s efforts to turn litigation financing into a science, by combing through court records that live in disparate databases, analyzing the success rates of specific lawyers and attempting to package and sell that information to investors.

Hedge fund gurus, too, are getting in on the game. Emmanuel Friedman, whose $6-billion fund profited handily from the TARP program, now wants in on litigation funding and is investing in class action suits over vaginal mesh failures, an unsettling phrase that you may have heard on late-night law firm commercials. Thanks to hedge-fund money, you’re going to hear it a lot more.

At the other end of the spectrum is Mighty, a company clearly inspired by Kickstarter, which takes a crowdsourced approach to litigation financing, offering a platform where individual investors (mostly other attorneys, according to company founder Joshua Schwadron) can pick and choose among potential cases in an online marketplace. Schwadron writes passionately about his company providing “power to the plaintiff,” who might be otherwise unable to afford justice. He also dangles the prospects of 30 percent annual returns on investment; but, in a marketplace like this, it’s easy to see people choosing to back lawsuits because a case pulled at their heartstrings, or simply on a whim.

It’s in this “heartstrings” category where Thiel’s backing of Hogan’s lawsuit more clearly lies. (As he told the Times, “This is not a business venture.”) A clear red flag in the case, of course, was when Hogan’s team dropped a claim that removed Gawker’s insurance company from the equation — eliminating the possibility of an easier settlement. As an investor Thiel, seems to have guided the case toward his primary goal — the destruction of the media company he loathes — as opposed to one that’s in a typical business person’s best interests. But that’s the rub with any form of litigation finance, whether you’re taking money from a hedge fund or a peeved billionaire: you might be plaintiff, but you’re no longer in the driver’s seat.

Josh Fruhlinger is a writer, editor and professionally funny person who lives in Los Angeles. He is a contributor at MEL and author of The Enthusiast, a book about trains, comics, stealth marketing, capitalism and joy.

{kind=link}

{kind=link}

{kind=link}